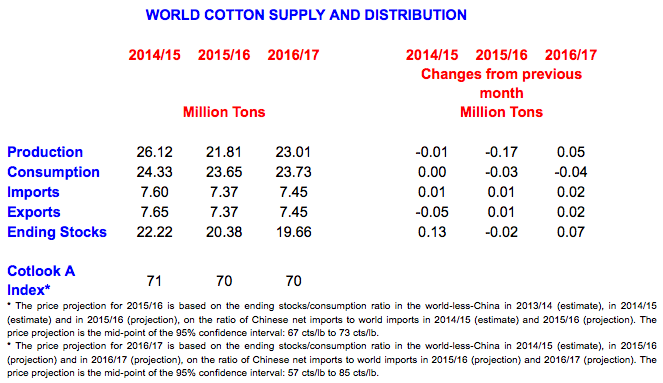

In 2015/16, world cotton consumption declined by 3% to 23.6 million tons and will likely remain at the same level in 2016/17 due primarily to low polyester prices and weak global economic growth. After reaching a record level of 10.9 million tons in 2007/08, cotton consumption in China has declined in each subsequent season with the exception of 2009/10.

However, China remains the world’s largest consumer and mill use is estimated at 7.1 million tons in 2015/16. High domestic cotton prices, particularly compared with those of polyester, are expected to cause China’s cotton consumption to decrease by 5% to 6.7 million tons in 2016/17. However, mill use is anticipated to increase in several other large cotton consuming countries, which would offset the decline in China. After falling by 3% in 2015/16 to 5.2 million tons, cotton consumption in India is expected to rise by 4% to 5.4 million tons in 2016/17 due to favorable textile export policies, well integrated downstream industries and competitive prices. After three seasons of growth bolstered by China’s demand for cotton yarn, mill use in Pakistan fell by 12% to 2.2 million tons in 2015/16 due to the ongoing energy crisis, high costs of production, and weak cotton yarn demand. Mill use in Pakistan is forecast to rise by 1%, to a little over 2.2 million tons in 2016/17. Bangladesh and Vietnam are projected to see significant growth in 2016/17, with mill use increasing by 16% to 1.3 million tons in Vietnam and 10% to 1.2 million tons in Bangladesh.

China began selling cotton from its national reserve last month as part of its efforts to reduce its large cotton stockpile. The total volume sold reached 450,000 tons as at the time of writing, which reduces the total volume in China’s reserve to around 10.6 million tons. Sales have been robust with nearly all domestic cotton and all imported cotton on offer being purchased. Imports by China are forecast to fall by 12% to 960,000 tons in 2016/17 due to the government’s desire to reduce its cotton reserve stock and restrict imports. However, imports by the rest of the world are expected to increase by 3% to 6.5 million tons, with Vietnam and Bangladesh emerging as the world’s largest importers, accounting for 34% of the world’s imports. World cotton imports are forecast to increase by 1% to 7.4 million tons in 2016/17. Exports from the United States are anticipated to rise by 11% to 2.2 million tons in 2016/17, due to increased domestic production and ample carryover stocks.

In 2015/16, world cotton production dropped by 17% to 21.8 million tons as world cotton area shrank and many countries experienced below-average yield. However, production is forecast to increase by 6% to 23 million tons as world cotton area expands and yields improve. India is likely to maintain its place as the world’s largest producer in 2016/17 and its production is projected to increase by 10% to 6.5 million tons. Production in China is expected to fall by 10% to 4.6 million tons due to reduced subsidies and high production costs.

World ending stocks are expected to decrease by 4% to 19.7 million tons by the end of 2016/17, which would follow an 8% reduction in stocks to 20.4 million tons in 2015/16. However, ending stocks outside of China are projected to rise by 3% to 8.8 million tons in 2016/17.

Source

International Cotton Advisory Committee, press release, 2016-06-01.

Supplier

International Cotton Advisory Committee

Share

Renewable Carbon News – Daily Newsletter

Subscribe to our daily email newsletter – the world's leading newsletter on renewable materials and chemicals