CAS, the Chemical Abstracts Service (a division of the American Chemical Society), keeps a listing of regulated chemicals around the world. It contains over 310,000 substances. This fact alone indicates that to talk about “the” chemicals market is a gross simplification.

Little wonder then, that companies looking in from outside find they are entering a far more confusing universe of different molecules, markets, applications, value propositions and supply chains.

This is proving particularly true for those from the “bio” industries, many of whom started life aiming at the relatively simple markets of fuel: “will it be ethanol or biodiesel today, sir?”

Sure, within this complexity there are big markets (“bulk” chemicals such as ethylene) and smaller ones (“fine” chemicals with longer, easily-forgettable names such as those found in pharmaceuticals and food additives), plus a whole range of “intermediates” in between.

So where to aim your business?

Big markets come with nice big numbers: depending whose forecasts you believe, the ethylene market may reach $180 billion within the next 3 years. Imagine securing even just a small percentage of that pie (achieving IPO and retiring to your tropical island…)?

Big markets come with nice big numbers: depending whose forecasts you believe…

But these markets also come with massive economies of scale: big volume plants (with huge capex requirements), driving low per-tonne production prices. And anyone who’s attended the series of “World Bio Markets” events over the last few years will know that taking clever biomass conversion processes to massive scale remains “problematic” (I understate…), particularly constrained by access to sufficient financing.

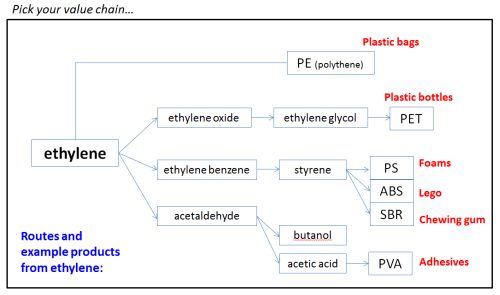

Bulk chemicals also tend to be just the start of a long and complex chain of processes; from ethylene (a gas) through to the polystyrene packaging protecting your shiny new TV, for example. So if you intend to drop your “bio”-ethylene into this chain, you’ll be hard-pressed to succeed (read: hoping in vain) unless you are cost-competitive with the petrochemical-derived alternative.

To play in this game then, you’ll need a deep-pocketed partner, a friendly “big chem”. But for how long will they remain friendly? Their investment may be life-changing for your business, but is it just small change to them? Are you one bet in a portfolio of similar bets, small enough that they can afford to quickly drop you if you lag behind or their priorities shift?

Hmm, sounds scary. So what about the speciality markets?

Ok, so these markets don’t look so vast (so maybe your tropical island in retirement will be smaller). But then the price-per-tonne numbers are much more attractive and there’s less of that pesky scale problem to overcome: a few tonnes per year may be enough.

Here we have the basis for a long-term, sustainable market – in the business sense, not just the “green” one.

If your clever industrial biotech process can go straight to a specialised, end-use molecule, particularly a novel one rather than substituting an existing one, your supply chain to the end market could prove to be much more direct. And if your end market is one where there may be significant “demand pull” (face creams, perhaps?), then your “bio” route may even demand a premium.

Wow! Imagine that? Charging more because consumers want your bio-product more, not because policy props exist to make it so? Here we have the basis for a long-term, sustainable market – in the business sense, not just the “green” one.

Ok, that all sounds great, now just need to understand which of those thousands of different speciality chemical markets you should target… And hope that those unpredictable consumers don’t suddenly shift their tastes.

These are of course two extremes: we haven’t even started on the array of molecules that fall somewhere in between, with lower scale-up requirements than bulk markets but more end-use flexibility than speciality ones (reminder: 310,000 registered substances!). Or even touched on the array of potential feedstocks and conversion processes from which to turn that chunk of plant material you can access into something useful you can sell.

Finally, remember that “bio-based” chemicals are nothing new: ethanol, oleochemicals, acetone and ascorbic acid are just a few examples dating back a century or more.

Ultimately the growth of new bio-based chemicals of whatever type, and the success of the clever firms that enable them, will be driven by their ability to offer specific market advantages, in particular one or more of: lower cost processes, improved and novel properties, demand-pull differentiation from their alternatives.

It is a brave person (or clairvoyant) who can say who will succeed and who will fail, so the only conclusion is that interesting times lie ahead. Good luck!

About Green Power Academy and Dr John Massey

Dr John Massey is lead trainer for the Green Power Academy and a writer on all things renewable.

The Academy runs a 2-day “Technologies & Markets for Biochemicals and Bioproducts” course. It provides a comprehensive analysis of biomass feedstock conversion technologies and the market growth opportunities for creating chemicals and other products. Available in-house or as a public course, with upcoming dates in London, Brazil and the US.

Source

Green Power Academy, press release, 2014-05-20.

Supplier

American Chemical Society (ACS)

Chemical Abstracts Service CAS

Green Power Academy

Institute of Process Engineering, CAS

Share

Renewable Carbon News – Daily Newsletter

Subscribe to our daily email newsletter – the world's leading newsletter on renewable materials and chemicals