The Chinese government announced a new target price for cotton grown in Xinjiang last month of 18,600 yuan per ton (approximately U.S. 122 cts/lb using current exchange rates), unchanged from 2016, and will be in effect through the 2019 planting season. In order to maintain a stable supply of cotton, the subsidy will also only apply to output less than 85% of the average annual production grown from 2012-2014 (around 7 million tons). The level of subsidy for extra-long staple cotton will remain unchanged at 1.3 times the price of upland cotton.

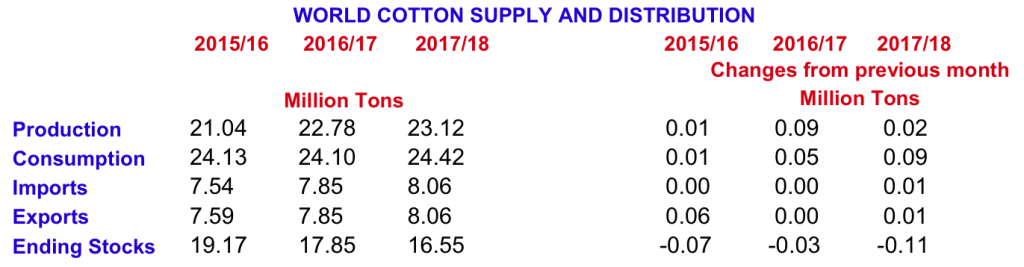

World cotton production is forecast to grow by 1% to 23.1 million tons in 2017/18 as high prices in 2016/17 encourage farmers to plant cotton. However, the average yield is expected to decline by 2% to 761 kg/ha, similar to the 4-year average. India’s production is projected to grow by 2% to 5.9 million tons while production in China could reach 4.8 million tons in 2017/18 as area expands by 3% to 3 million hectares after five seasons of contraction. High yields and firm prices will encourage farmers in the United States to expand d cotton area in 2017/18. However, production is expected to remain unchanged from 2016/17 at 3.8 million tons as the average yield is assumed to be closer to the 5-year average.

World cotton mill use in 2016/17 is expected to remain unchanged at 24.1 million tons due largely to weak global economic growth and competition from polyester. Global consumption may recover by 1% in 2017/18 to 24.4 million tons as cotton prices decrease, and growth in the global economy is expected to be much stronger in 2017 and 2018. After several seasons of decline, China’s mill use is projected to rise by 2% to 7.6 million tons in 2016/17 and by 1% to 7.7 million tons in 2017/18. The gap between China’s domestic cotton prices and international cotton prices has decreased, making yarn imports less attractive than in recent seasons. In addition, mill use in Xinjiang has expanded, and the proximity to the higher quality cotton grown in this region offers cost advantages over yarn imports. After declining by 3% to 5.1 million tons in 2016/17 due to high domestic and international cotton prices, India’s mill use is projected to recover by 1% to 5.2 million tons in 2017/18.

During the first seven months of 2016/17, China has imported over 600,000 tons of cotton, up by 6% from last season during the same time period. China’s total volume of imports is expected to rise by 2% to 983,000 tons in 2016/17. Imports by Bangladesh are expected to rise by 6% to 1.4 million tons, and Vietnam’s imports are projected to grow by 17% to 1.17 million tons in 2016/17. Given its large exportable surplus and the high quality of its crop this year, the United States is expected to export 2.9 million tons of cotton in 2016/17, accounting for 37% of global exports. India’s exports are projected to decline by 23% to 960,000 tons in 2016/17, partially due to the delay in harvesting earlier this season while China began selling cotton from its national reserve last month, and as at the time of writing, total volume sold reached 450,000 tons. If the level sales that occurred last month continue, a similar volume of cotton may be sold this year as well, bringing the total volume held by the government to around 6 million tons at the end of August 2017. At the end of 2016/17, China’s stocks are projected to fall by 17% to 9.3 million tons. World ending stocks in 2016/17, are expected to decline by 7% to 19.1 million tons.

Source

International Cotton Advisory Committee, press release, 2017-04-03.

Supplier

International Cotton Advisory Committee

The State Council of the People's Republic of China

Share

Renewable Carbon News – Daily Newsletter

Subscribe to our daily email newsletter – the world's leading newsletter on renewable materials and chemicals