The global biofuels market is comprised of a veritable potpourri of regional outcomes, driven by government mandates, feedstock availability, VC largesse, concerns around energy and/or food security and a mix of outright myopic stupidity and agendas. The good news is that data and analysis thereof can always be used to drown out the noise and make sense of the signal.

The global biofuels industry averaged 68% in utilization rate from 2005 to 2014, reaching a high of 80.9% in 2007, dropping to a low of 56.9% in 2012, and climbing slightly back to 60.4% in 2014. Despite the still apparent softness in capacity utilization, and the on-going softness in fossil fuel prices, global biofuels capacity will continue to grow from 55.1 billion gallons per year (BGY) to 61.4 BGY in 2018, but the growth between now and then will not be a continuation of current course. While ethanol and biodiesel will continue to dominate in absolute terms, these will grow at only a 1.5% CAGR through 2018. Novel fuels and feedstocks will drive the biofuels industry forward at a much more rapid 17% and 22% CAGRs through 2018, respectively.

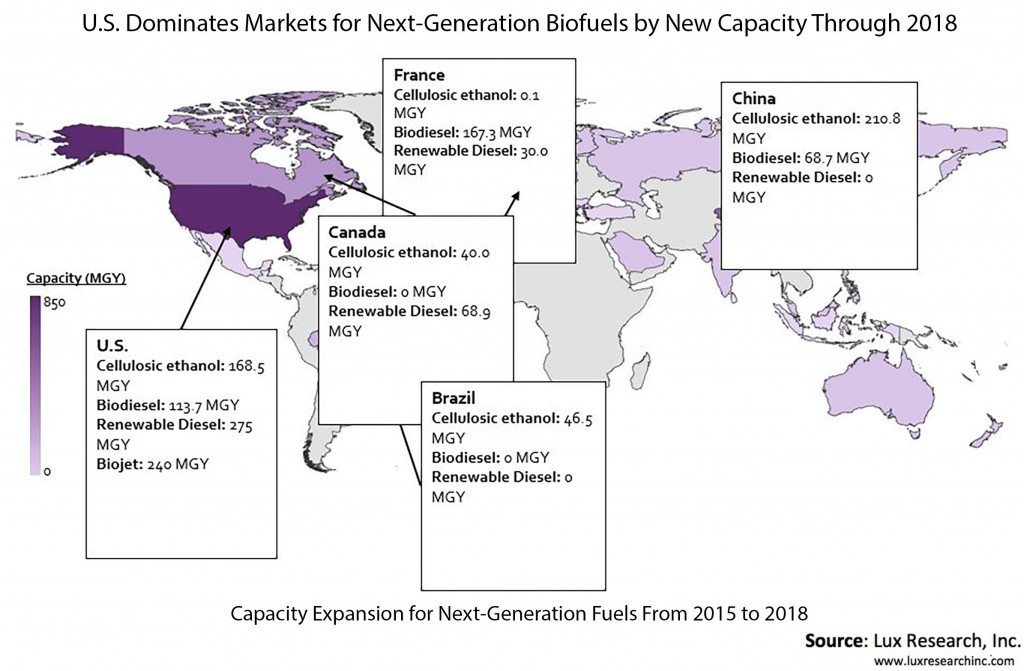

Next-generation biodiesel leads capacity in 2018 for novel fuels making up 56% (2.7 BGY). With the ongoing “Food vs. Fuel” debate, the use of vegetable oils has been capped in regions like the EU. Waste oils (corn oil, yellow grease, brown grease, and mixed oils), on the other hand, will emerge as a leading feedstock choice and account for 61% of next-generation biofuels with a 3.0 BGY capacity in 2018. However, economically aggregating large quantities of feedstock remains a major barrier because of decentralized distribution. Cellulosic ethanol and renewable diesel represent the next largest shares with 19% (904 MGY) and 14% (690 MGY) of total next-generation fuel capacity in 2018, respectively. China, U.S., and Brazil lead cellulosic ethanol expansion representing 35%, 27%, and 10% of capacity in 2018, respectively. While commercial-scale cellulosic ethanol became a reality in 2014, feedstock logistics also remain a major barrier for these developers. Renewable diesel faces numerous barriers as well. While companies like Neste, Renewable Energy Group (REG), and Diamond Green Diesel have shown commercial promise in 2014, they will compete with next-generation biodiesel for the same feedstocks.

As feedstock is a critical factor in both the economics and scale up of biofuels, companies will need to implement innovative supply chain strategies to beat out competitors. For example, UPM mitigates feedstock risks by tapping into its own tallow oil supply and Diamond Green Diesel secures animal fat through joint venture partner Darling Ingredients. Others sitting on robust feedstocks also have significant power to control where investment in biofuel capacity occurs, but need to think about partnerships sooner rather than later. Downstream users also need to be ready to act and know where to act. Biojet fuel has seen some remarkable partnership development across the entire value chain given the relative infancy of the technology, with major airlines already taking a significant interest in developers including announcing test flights, investments, and strategic partnerships. The likes of Cathay Pacific, United Airlines, and Southwest Airlines have entered off-take agreements with their respective developers, locking in significant quantities of biojet fuel for the next 10 years.

Biofuels are still not a field of dreams wherein “if you build it, they will come”, but there are opportunities for growth if the right strategies are derived from accurate date to build capacity that makes sense for the long haul.

Source

Lux Research, press release, 2015-08-29.

Supplier

Cathay Pacific Airways

Darling Ingredients

Diamond Green Diesel

Lux Research, Inc.

Neste Oil

Premium Renewable Energy Group

Southwest Airlines

United Airlines

University Putra Malaysia (UPM)

Share

Renewable Carbon News – Daily Newsletter

Subscribe to our daily email newsletter – the world's leading newsletter on renewable materials and chemicals